RUPEE COST AVERAGING AND COMPOUNDING IN MUTUAL FUNDS:A Beginner’s Guide To SIP And More

- Mon Aug 11 18:30:00 UTC 2025

- In mentoring and guidance by Aparna Bose

When you invest in Mutual Funds, two powerful concepts work together to help your wealth grow: Rupee Cost Averaging (RCA) and Compounding.

Rupee Cost Averaging (RCA) is a simple yet effective strategy—perfect for Systematic Investment Plans (SIPs). You invest a fixed amount at regular intervals, regardless of market ups and downs. When the Net Asset Value (NAV) is low, you buy more units; when it’s high, you buy fewer. Over time, this smooths out the cost per unit and reduces the risk of investing a lump sum at the wrong moment. Think of it like consistently buying groceries—you pay less when prices dip and more when they rise, but overall, you get a fair average price. Easy and comprehensible, right?

Compounding is where the real magic happens. It’s the process of your returns generating their own returns—also called the "interest on interest" effect. When your earnings stay invested, they start producing additional earnings, creating a snowball effect. The longer you remain invested, the faster and larger your money can grow—turning time into your greatest ally.

So together, rupee cost averaging helps you invest steadily, and compounding helps your money grow over time. If you start early and stay invested regularly, these two strategies can help you build wealth in a simple and stress-free way.

Let’s explore an intriguing question: Have you ever thought about increasing your wealth without working harder for it? Maybe you’re concerned about accumulating enough for retirement or funding your child's education. Are you envisioning an early retirement, perhaps at fifty or fifty-five?

To address these important considerations, let’s dig deeper into the subject.

TIMING

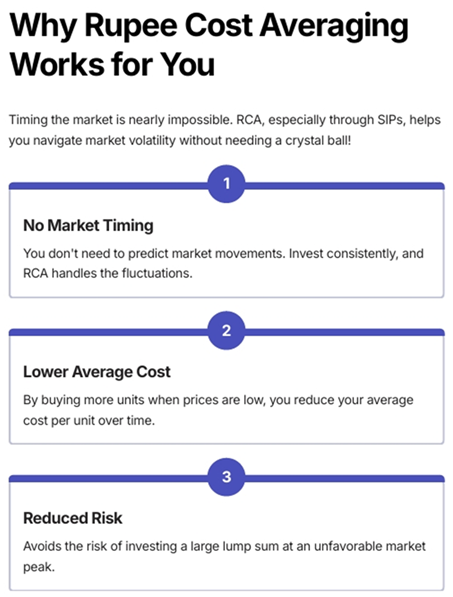

Timing the market accurately is a difficult task which is rarely accomplished on a consistent basis. However, the good thing is that you don’t need to have a crystal ball to earn profits. Market volatility is part and parcel of equity investments, reflecting the ups and downs of the economy. If you recall the law of demand, it says that a higher quantity of a commodity is purchased when it is least expensive. Conversely, the demand reduces when the price of the commodity increases.

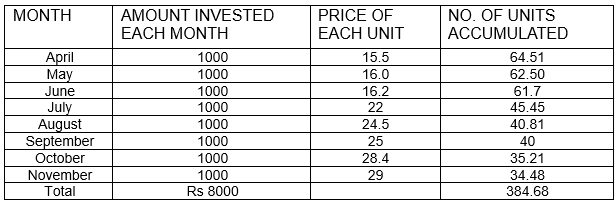

Let's take an example. A person invests a fixed amount of Rs 1,000 on the fifth of each month with a SIP in a mutual fund scheme. Let’s see what happens when the market oscillates:

If the same investor had invested Rs 8,000 as lump sum in let us say October instead of starting in a disciplined manner in April itself, then he/she would have procured 281.69 units . Even a lumpsum if invested for a long-term can perform as per your expectation and meet your investment goals but for the young and the disciplined, SIP is the best option always.

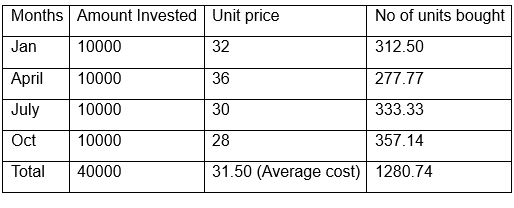

Let us take another example to demonstrate how does Rupee Cost Averaging work!

If the entire amount of Rs.40,000 is invested in January, the number of units bought would be 1,250, as compared to 1,280 units acquired at the end of the year. Here’s where SIP allows an investor to reap the benefits of rupee cost averaging.

To summarize, Rupee Cost Averaging implemented through a systematic investment plan enables you to manage market unpredictability very effectively. However, it should not be taken as a guarantee to earn profits as all equity-oriented investments are subject to market risk. To ensure that you gain the most from Rupee Cost Averaging and SIPs, you need to invest continuously over the long term.

Please consult our experts at Investaffairs to know more on Rupee Cost Averaging.

BENEFITS OF INVESTING IN SIPS

Check out the various benefits of choosing to invest in an SIP:

- SIPs are quite easy options for beginners and for disciplined investors.

- SIPs can be started with even small amounts like Rs.1000 or Rs.2000 every month so that you do not have to burden yourself.

- With SIPs, you can build your funds over time without much effort as they allow you to get decent funds with time with the help of compounding.

- SIPs also bring discipline by encouraging regular savings and protect you from market ups and downs through rupee cost averaging.

- They are flexible which means you can increase, pause, or stop your SIP anytime

There is a simple way to accomplish all these things if you are willing to learn how to put your money to work for you. It is called compounding, and it can help you exponentially grow your money over a period of time.

THE POWER OF COMPOUNDING: HOW TO MAKE YOUR MONEY WORK FOR YOU

Compounding can be a powerful tool for mutual fund investors, as it can lead to significant growth in the value of an investment over time. However, it is important to keep in mind that past performance is not necessarily indicative of future results and that the value of an investment can decrease as well as increase. Additionally, investors should also consider the risks, charges and expenses of a mutual fund before investing.

Unlike simple interest—where you earn returns only on your original investment—compound interest grows your money by reinvesting the returns you earn, allowing your investment to snowball over time.

WHY TIME IS YOUR BEST FRIEND?

Time is the true engine of compounding. The longer your money stays invested, the more exponential its growth. For instance, here’s how a ₹10 lakh investment can expand over various time periods at a 10% annual return:

Over 30 years, your investment grows over 17 times its original value. But if you had invested for only 20 years, you’d have earned just 6.6 times your principal. That’s the true power of compounding—TIME AMPLIFIES GROWTH.

RECAP

Disclaimer: The data and information has been sourced from various domains available to the public. We have taken utmost care to represent the same as factually as has been made available. Please do not make any decisions based on our blogpost. Kindly check the data & information independently. For further guidance on finance and investment please reach out to our experts at Investaffairs.

If you have any Personal Finance query, do write to us

Categories

Recent Posts